Can Companies Catch Up to the Advancement in Supply Chain Technology?

Today, nine out of ten supply chains are stuck. Despite two decades of advancement in supply chain technologies, companies are struggling to gain balance at the intersection of operating margin, inventory turns and case fulfilment.

Market volatility is increasing and supply chains can respond, but they cannot sense. They are slow to adapt.

Over the course of the last year, I have written about this extensively. The research that I have conducted has enabled me to look at this holistically. For me, this has been discovery.

I am an old gal. Like an artifact, I have kicked around in the supply chain space since the 1980s. I believed that the first generation of supply chain systems would improve operations to a greater degree than actually happened. As an analyst, I had predicted great things that did not happen. Recently, I did a mea culpa. I am sorry.

As a result, I am trying to be more careful to not overhype the market. When I left AMR Research I invested over 400K in building a database of supply chain financial ratios to correlate supply chain results. My goal is to understand the impact of technologies and processes. It is easier said than done. After three years of research, I have just refined the methodology to start to pull the trends.

I have learned that supply chain systems are more complex than I originally thought, and that the relationships between supply chain metrics are nonlinear. I have also learned that you need a large data pool to derive the type of analysis that I want to publish. It takes more than one or two respondents from a company.

I need to finish the work, but in the process—like the Hippocratic Oath above—I want to do no harm.

Why It Matters

Today, we have a number of burning platforms. Recently, I spoke to a major European retailer that lost 5% of their grocery revenues to Amazon in the first quarter of 2014. It is clear to them that Amazon is going to be anything that they want to be, and that they need to defend their turf. In a similar vein, a major 3PL that I spoke to last week at Eye for Transport is considering discontinuing the traditional storage of spare parts and initiating a new service to do 3D printing of parts on demand. There are many tipping points happening together, and companies want to know what can drive the greatest value.

What I See in the Data

In my work on the Supply Chain Index, I see that companies I recognize as doing network design well are rising faster on the list of the Supply Chain Index work. The network design technologies have changed a lot in the last decade. (I sometimes wonder if I should create a new class of technologies for the network design tools because they have changed so much.) The older tools from CAPS Logistics, SNO from Oracle, and Manugistics Network Planning are giving way to new technologies like the Logictools product (purchased from IBM), the Solvoyo product for concurrent planning, the Quintiq technology for concurrent optimization, and the Llamasoft technology platform for optimization and simulation.

These technologies are applicable to solve many problems. These tools allow us to look at sell, source, make, and deliver together. They also enable the evaluation of networks for both sales and procurement relationships to optimize the flows upstream and downstream. The technologies enable the evaluation of both volumetric flows and cost. And optimization, as well as simulation, can now be done together.

I am a big fan of the use of these types of technologies. The work on the Supply Chain Index shows me that the companies that I consider to be the most mature in the use of these technologies—General Mills, Intel, Cisco, and Seagate—are outperforming their peers. Is it coincidence? I don’t think so. I think that it matters.

Next week I will be speaking at the Llamasoft Summercon conference (follow this link to see the slides). On October 15th, I will be speaking on the Qunitiq World Tour in Philadelphia. Along the way, I will be doing more work on network design case studies. In preparation for these speeches, I have recently completed some quantitative research on network design. Here I share a cut of the data.

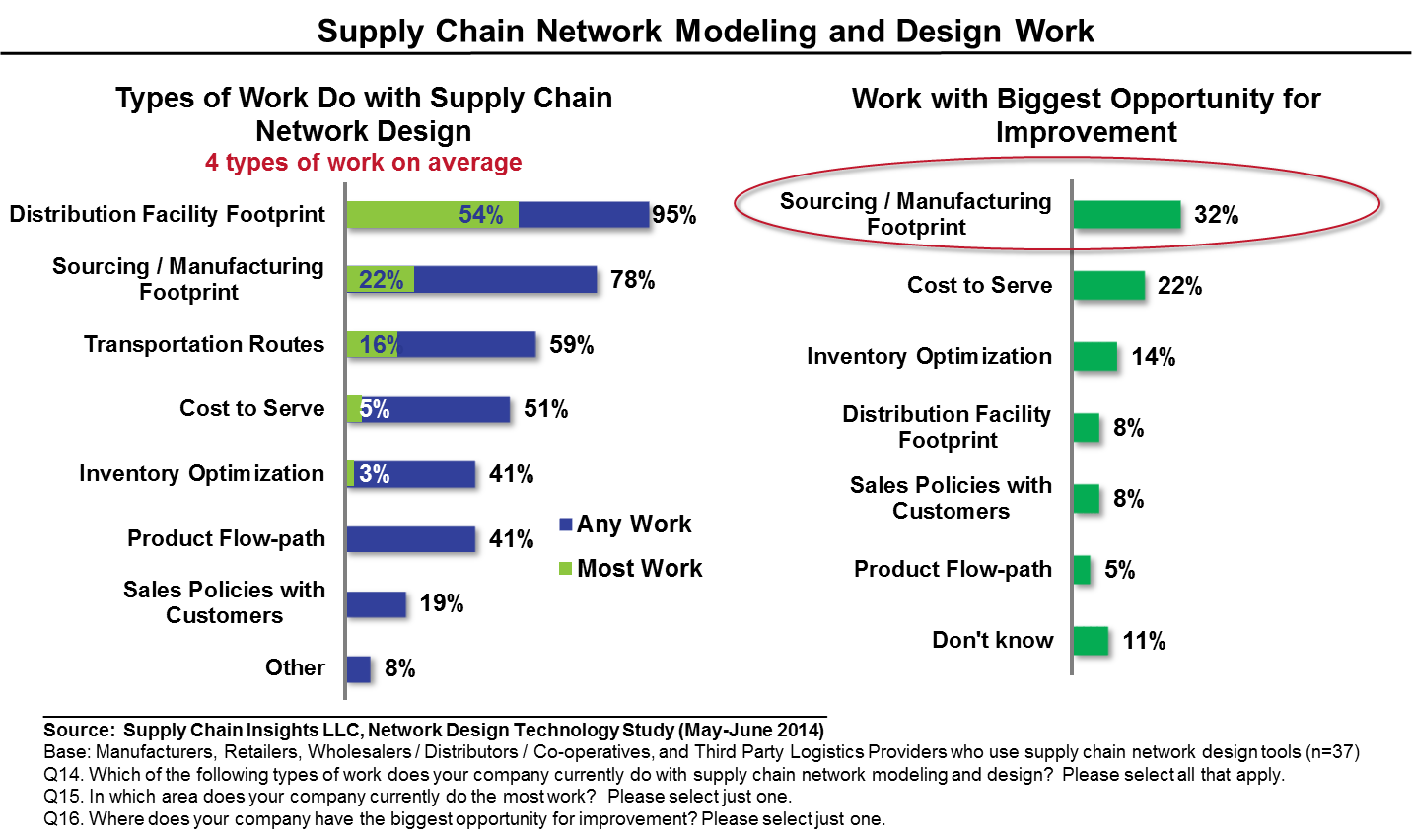

Figure 1.

Where Would I Start?

In figure 1, from the research, I share the current state of network design usage. As you can see from the data, while companies have increased the frequency of network design work from yearly to quarterly, most of the work is still focused on basic network design. The focus is on physical assets. I feel that the opportunities are in flows. The greatest gap is in the design of supplier and manufacturing networks. I also think that there is a great opportunity for increased focus on flow-path analysis and a shift from optimizing inventory levels to optimizing the form and function of inventory in value networks.

Anyway, in my effort to do no harm, this week, in a series of blog posts, I outline what I would do if I was a supply chain leader managing a company that was stalled at the intersection of inventory turns and operating margin. My first investment would be in network design to holistically design the network. I would not stop with the physical design. Instead, I would look at network flows, the form and function of inventory, cost-to-serve analysis, and the determination of the supplier network. I would infuse it into S&OP, risk management, and supplier development. I would build an expertise system in the Supply Chain Center of Excellence. I believe that it matters. While there are many factors that affect corporate performance, I can see that the leaders in the implementation of network design technologies are rising up the ranks on the Index and outpacing their peers.

If you are interested in some of our other studies on supply chain planning excellence, consider participating in our study on Supply Chain Planning: Is Faster Better. And, in ourDigital Manufacturing Study. Both of these studies are slated to close in a week to be available for our July newsletter. Companies participating in the planning study will be able to benchmark the number of planners needed by supply chain complexity and better evaluate the rate of implementation. In contrast, the digital manufacturing study evaluates the rate of adoption of new technologies like The Internet of Things and 3D printing to change manufacturing strategies. As always, when you give to us, we give to you. We never release the names or the individual responses of the respondents, but we always share the results in aggregate and offer a one-hour call for those that want to better understand the data.